This is part of an ongoing series about property revaluation in Jersey City. Note: this post presumes an understanding of the equalization ratio, which I previously wrote about in “Property Revaluation 101: the Equalization Ratio.”

With Jersey City officials recently announcing that they would finally move forward with a property revaluation, a common question has emerged: “is my home currently under-assessed, over-assessed, or fairly assessed?” It’s an important question for many reasons, including:

- If you are currently over-assessed, you may be eligible to win a tax appeal, thus shaving tax expense off your annual home ownership bill (tax appeals are generally due on or before April 1st each year). Also, you may see tax relief post-revaluation.

- If you are currently under-assessed, you will likely see a tax hike post-revaluation.

So…how do you figure out if you’re currently under, over, or fairly assessed? I’ve created three examples below to illustrate the math and logic.

Let’s get civic.

A Primer: Civic JC’s “Property Taxes 101” Forum

I first learned about tax appeal math at the “Property Taxes 101” workshop hosted by local good government group Civic JC. The workshop was presented by Thomas M. Olson, a real estate attorney from Morristown, NJ. The entire event is viewable below and dives into a lot more nuance than I’m covering in this post. On the topic of tax appeals, Mr. Olson referred to “Chapter 123,” which is a formula that “tests the fairness of an assessment.”

After attending the workshop, I read Chapter 123 and visualized the logic in Excel. That logic, and the accompanying visual, is what I’m sharing below.

Assessment Lingo & Numbers: Chapter 123 Law Terminology

To understand this topic, we need to get grounded in two sets of numbers: city-specific numbers and property-specific numbers.

Here are the city-specific numbers:

- Equalization Ratio: Every municipality in NJ has an equalization ratio, published each year here. In Jersey City, the 2016 equalization ratio is 27.63%, meaning assessed values are, on average in Jersey City, 27.63% of market values.

- Common Level Range: The common level range is defined as “plus or minus 15% of the average [equalization] ratio” … the +15%/-15% is like wiggle room around the average equalization ratio…akin to a margin of error in a poll.

- Upper Limit: This is the top of the common level range. The formula for the Upper Limit is: Equalization Ratio * 1.15.

- Lower Limit: This is the bottom of the common level range. The formula for the Lower Limit is: Equalization Ratio * 0.85.

Here are the property-specific numbers (these are specific to your home):

- Assessed Value: This is available at the NJ County Tax Boards website here.

- Market Value: You can obtain this from a local realtor.

If you are not familiar with assessed versus market value, I recommend another article I wrote in this series, “Property Revaluation 201: Quantifying Tax Inequity (Part 1 – A Simple Example),” which explains how market and assessed values can change over time.

Property Assessment Math: Some Examples

The state of NJ publishes examples of the Chapter 123 test each year, as well as an informing “Guide to Tax Appeal Hearings.” Both of these resources are helpful because they explain the math and the process underlying tax appeals. I’ve modeled the examples below off the state’s examples. Note that for each example, we will go through two steps:

- Define the dollar-value Common Level Range for the property.

- Determine if the Assessed Value falls below, above, or within the Common Level Range.

Note: “house” is interchangeable with “property” below.

Example #1: An OVER-Assessed Property.

Market value = $200,000 and assessed value = $100,000.

Step 1: Define the dollar-value common level range for this house:

- The top of our common level range is our upper limit (31.77%) times market value ($200,000) = $63,549.

- The bottom of our common level range is our lower limit (23.49%) times market value ($200,000) = $46,971.

Step 2: Determine if assessed value is above the upper limit ($63,549) or below the lower limit ($46,971).

Conclusion: Because the house’s assessed value of $100,000 is more than the upper limit of $63,549, this home is over-assessed. The assessment could be corrected DOWN to $55,260 ($200,00 market value times the average ratio of 27.63%). The taxpayer’s tax bill would in turn be reduced by $3,347.

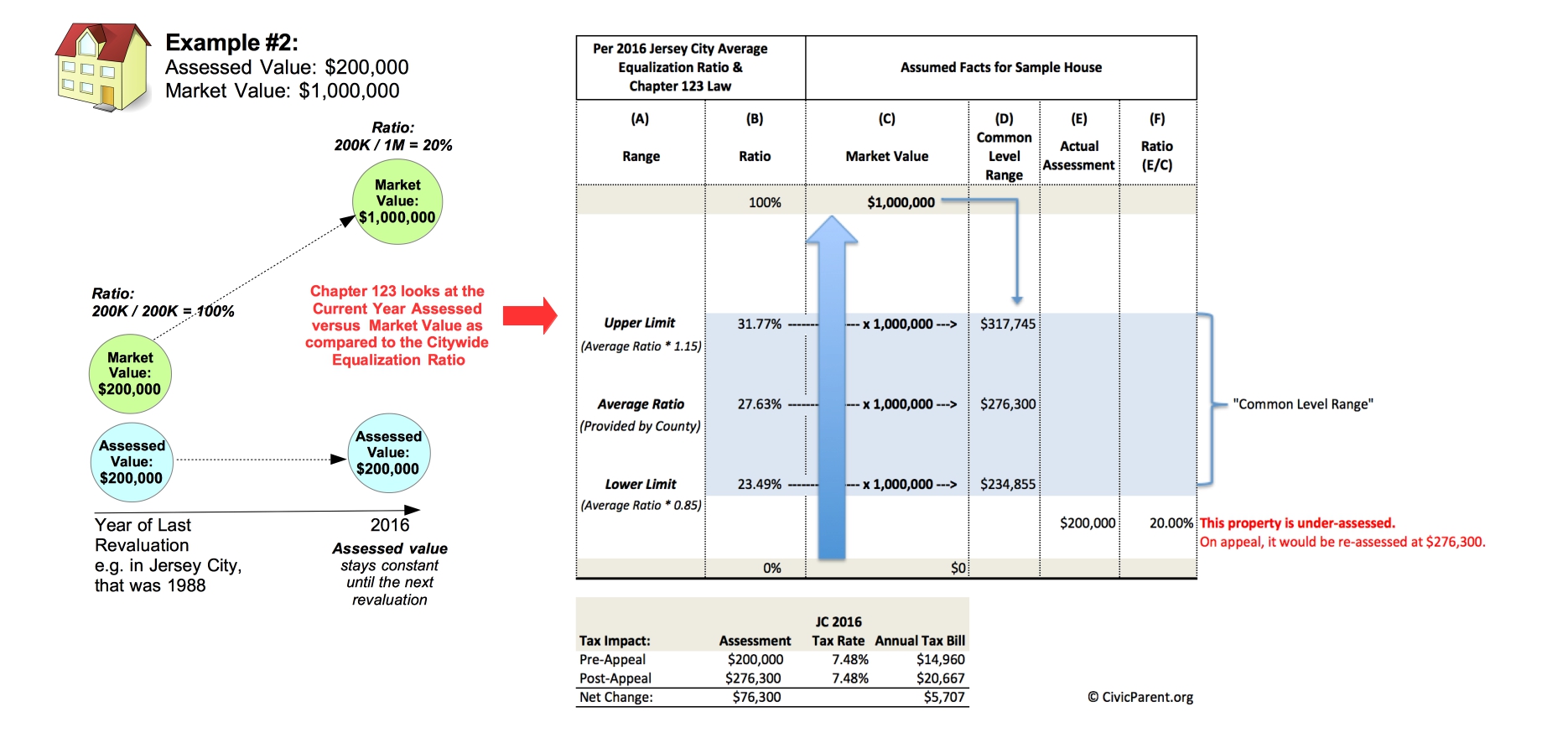

Example #2: An UNDER-Assessed Property.

Market value = $1 million and assessed value = $200,000.

Step 1: Define the dollar-value common level range for this house:

- The top of our common level range is our upper limit (31.77%) times market value ($1,000,000) = $317,745.

- The bottom of our common level range is our lower limit (23.49%) times market value ($1,000,000) = $234,855.

Step 2: Determine if assessed value is above the upper limit ($317,745) or below the lower limit ($234,855).

Conclusion: Because the house’s assessed value of $200,000 is less than the lower limit of $234,855, this home is under-assessed. The assessment could theoretically be corrected UP to $276,300 ($1 million market value times the average ratio of 27.63%). The taxpayer’s tax bill would in turn be increased to $20,667.

Example #3: A FAIRLY Assessed Property.

Market value = $500,000 and assessed value = $150,000.

Step 1: Define the dollar-value common level range for this house:

- The top of our common level range is our upper limit (31.77%) times market value ($500,000) = $158,873.

- The bottom of our common level range is our lower limit (23.49%) times market value ($500,000) = $117,428.

Step 2: Determine if assessed value is above the upper limit ($158,873) or below the lower limit ($117,428).

Conclusion: Because the house’s assessed value of $150,000 is within the lower and upper limits, i.e. within the common level range, it is considered fairly assessed. There would be no change to the assessed value.

What About Your House?

To figure out your specific facts and circumstances, run through the same steps as above:

- Define the dollar-value common level range for your house.

- Determine if your assessment value is below, above, or within the Common Level Range.

Then…analyze the results:

- If your assessed value is above the upper limit, you’re over-assessed.

- If your assessed value is below the lower limit, you’re under-assessed.

- If your assessed value is within the common level range, you’re fairly assessed.

The math is relatively straightforward, but it represents only one step in the overall appeal process. To learn more about the process of appeals, click here.

What about Revaluation?

When the city conducts the revaluation (likely to be a multi-year process), assessed values will be updated to equal market values and the equalization ratio will reset to 100%. The common level range will no longer be necessary. Until, that is, the city’s equalization ratio dips below 85% at some point in the future…then taxpayers will need to re-engage Chapter 123 and the case for revaluation would again start to take shape.

Further Reading

Here are some resources that provide additional information:

- A Guide to Tax Appeal Hearings

- 2016 Common Level Range Certification (with examples) published by NJ Dept of Treasury

- Common Level Ranges – tables published by NJ Dept of Treasury

Interesting. According to this math, at my estimated ‘market value’ (based on a similar sale within the building) my assessed value is within the range (barely, at the top end) and therefore wouldn’t change. If I use the market value when I bought my condo 2 years ago, the assessed value is well above the range and should be corrected down. In either case, it seems like I’m looking at no change or slight decrease in taxes then? That’s reassuring.